Latest Posts

Here's a situation we often find ourselves in a loved one's birthday or graduation is coming up, or another holiday is around the corner, and we're struggling to think of a meaningful gift that will really show our loved ones we care. While most people resort to fad toys, clothes youngsters will quickly outgrow, and Amazon purchases people will soon forget, consider making your birthday, graduation, or holiday gift one that will last for years and positively impact your loved ones' futures. Enter, a 529 plan.

What is a 529 Plan?

A 529 plan is an investment account specifically designed for educational savings for a beneficiary, the individual for whom the account is created for. When it comes to gifting, family members, friends, and loved ones can either make contributions to a 529 account that has already been set up in the recipient's name, or they can set up a 529 account for the beneficiary and fund it with their desired gift amount, as there is no minimum to open or contribute to these accounts. Additionally, an important feature of 529 plans that many people overlook: There is no age limit for a beneficiary. This means an adult can be the beneficiary; for example, maybe he or she plans to complete an unfinished degree, pursue a graduate degree, or is an expecting parent who can change the newborn to be the beneficiary upon the baby's arrival.

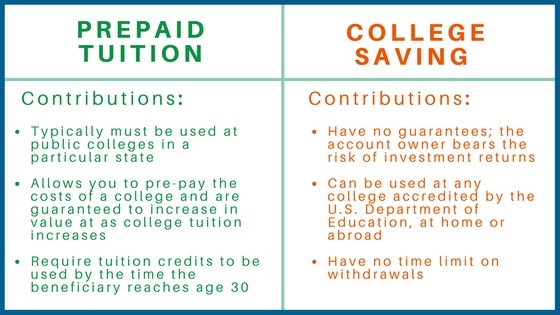

There are two types of 529 plans: college savings plans and prepaid tuition plans. College savings plans allow you to invest contributions to withdraw in the future for qualified education expenses, while prepaid tuition plans allow you to purchase college credits at today's prices to be used in the future. Prepaid tuition plans are more restrictive than savings plans in that they cannot be used for K-12 education costs or room and board, and prepaid plans may involve restrictions that limit which institutions they may be used for. Almost every state has at least one 529 plan option, and there is even a 529 plan managed by a group of private colleges and universities. Regardless of the option(s), you select, all 529 plans have significant benefits that make them the gifts that keep on giving. Here are three reasons why a 529 plan is the ultimate gift to give, no matter what the occasion may be.

Flexibility

These accounts are not only for the typical four-year college and university tuition costs. 529 accounts can also be used to fund trade and vocational schools, community colleges, graduate schools, and any institutions that participate in the U.S. Department of Education's student financial aid programs. Additionally, as a result of the 2017 Tax Cuts and Jobs Act (TCJA), 529 funds – up to $10,000 per child annually – can be used for kindergarten through 12th-grade tuition; however, note that not all states allow for this, but Maryland, Virginia, and D.C. do allow it. 529 funds are also eligible for additional qualified higher education expenses that are not included in tuition like fees, books, supplies, and even room and board if the student is enrolled at least part-time.

Although 529 accounts can only have one beneficiary at a time, meaning distributions from the account can only be used to pay for qualified expenses incurred by that one beneficiary, the owner of the 529 accounts can easily update the beneficiary of the plan if needed. For example, if the original beneficiary is fortunate enough to receive a full ride to school, you may easily change the plan beneficiary to a qualified family member without tax consequences. A few examples of qualified family members include another child, spouses, nieces or nephews, and siblings. Additionally, if a beneficiary chooses to follow another path besides continued education, the plan can be easily passed on to a suitable family member.

Tax Benefits

The distinguishing incentives that set 529 plans apart from other investment accounts are the tax benefits the account owner has when making tuition payments. Many states offer residents a deduction or credit (subject to limitations) for contributions to the state's plan, and some states even allow you to deduct contributions to any state's plan. You are not restricted to investing in your state's 529 plan(s), so it is important to shop around and know your options and the different tax advantages you can leverage. Additionally, 529 funds benefit from federal and state tax-free growth, and qualified withdrawals are tax-free. Similar to an individual retirement account (IRA), earnings on contributions to a 529 plan are tax-deferred; however, unlike a traditional IRA, distributions from the 529 plan are exempt from federal income tax if used for qualified expenses. All but seven states offer a full or partial income state tax deduction on contributions made to a 529 plan, and many states offer their own incentives for opening a 529 plan through the plan owner's home state.

It is important to note that when the original account owner contributes to a 529 plan, the assets remain in his or her control. When it is time to distribute the funds to pay for the beneficiary's education expenses, the original owner has the ability to control when distributions are made and for what purpose. This means that he or she can take withdrawals for personal use at any time; however, the earnings portions of any non-qualified distributions are subject to income taxes and a 10% penalty.

Growth Potential

A 529 plan provides an easy, hands-off method to save for future education expenses. Once you find the appropriate plan for your needs, the enrollment process is simple and straightforward. The plan assets are professionally managed and funds are typically invested based on the anticipated year the funds will be needed for education expenses. This helps ensure your contributions take full advantage of potential market growth. As the beneficiary of the account ages, the funds in the account have the opportunity to grow just as they would in a typical investment account with an added incentive: All 529 plan funds benefit from tax-free growth. Once your 529 is set up, you do not need to touch the plan until it's time to begin taking distributions, unless you need to make any changes to the beneficiary.

The SECURE Act and 529 Plans

The SECURE Act (Setting Every Community Up for Retirement Enhancement Act) was signed into law on December 20, 2019, and one of the bill's 29 provisions expanded the usage of 529 plan funds. This said provision allows tax-free distributions from 529 plans for qualified student loan payments, known as qualified education loan payments, to be used to pay down the principal and interest of a qualified education loan. Note that there is a $ 10,000 lifetime limit in terms of the amount of 529 funds an individual can use towards loan repayments. This provision applies to distributions made after December 31, 2018, and all withdrawal requests intended to be used towards a qualified loan expense must be made within the same calendar year in which the expense was incurred. This additional use of 529 plan funds is especially beneficial given the ability to change the beneficiary of these accounts. For example, if the original beneficiary receives a scholarship and no longer needs the funds, he or she can switch the beneficiary designation to a sibling or a relative who has student loans and can use up to $10,000 in the 529 account towards those repayments.

Final Thoughts

Education and particularly college expenses can be a significant burden for parents and loved ones, but a 529 plan helps manage that load and eases the stresses associated with the education-funding process. A 529 plan is free and simple to start: Research plan options, select either prepaid tuition or college savings plan, assign a beneficiary, and begin making contributions. Furthermore, these plans are controlled on the state level, and you are not limited to the options in your state; you are free to shop around and determine which state's plan is best suited for you. Each state has specific options available, so ensure you do the necessary research to determine which 529 plan best fits your budget. That being said, with the many options available, it's important to consult your financial advisor to discuss your needs and learn how the right 529 plan can help you achieve the education savings goals for your desired beneficiary. The next time you find yourself browsing Amazon for that perfect holiday, birthday, or graduation present, consider going the 529 route to give a gift that will really make a difference.

Disclosure: The fees, expenses, and features of 529 plans can vary from state to state. 529 plans involve investment risk, including the possible loss of funds. There is no guarantee that a college-funding goal will be met. In order to be federally tax-free, earnings must be used to pay for qualified higher education expenses. The earnings portion of a non-qualified withdrawal will be subject to ordinary income tax at the recipient’s marginal rate and subject to a 10 percent penalty. By investing in a plan outside your state of residence, you may lose any state tax benefits. 529 plans are subject to enrollment, maintenance, and administration/management fees and expenses.